Packages

These packages are available for use in your project. Scroll down for more information and links to the associated repository for each one.

|

Easily work with standard tables and parametric models with common survival calculations. |

Insurance, annuity, premium, and reserve maths. |

|

Robust and fast calculations for |

Meeting your exposure calculation needs. |

|

Composable contracts, models, and functions that allow for modeling of both simple and complex financial instruments. |

Easy-to-use scenario generation that's FinanceModels.jl compatible. |

For consistency, you can lock any package in its current state and not worry about breaking changes to any code that you write. Julia’s package manager lets you exactly recreate a set of code and its dependencies. More information.

Adding and Using Packages

There are two ways to add packages:

- In the code itself:

using Pkg; Pkg.add("MortalityTables") - In the REPL, hit

]to enter Pkg mode and typeadd MortalityTablesMore info can be found at the Pkg manager documentation.

To use packages in your code:

using PackageNameMortalityTables.jl

Hassle-free mortality and other rate tables.

Features

- Full set of SOA mort.soa.org tables included

survivalanddecrementfunctions to calculate decrements over period of time- Partial year mortality calculations (Uniform, Constant, Balducci)

- Friendly syntax and flexible usage

- Extensive set of parametric mortality models.

Quickstart

Load and see information about a particular table:

julia> vbt2001 = MortalityTables.table("2001 VBT Residual Standard Select and Ultimate - Male Nonsmoker, ANB")

MortalityTable (Insured Lives Mortality):

Name:

2001 VBT Residual Standard Select and Ultimate - Male Nonsmoker, ANB

Fields:

(:select, :ultimate, :metadata)

Provider:

Society of Actuaries

mort.SOA.org ID:

1118

mort.SOA.org link:

https://mort.soa.org/ViewTable.aspx?&TableIdentity=1118

Description:

2001 Valuation Basic Table (VBT) Residual Standard Select and Ultimate Table - Male Nonsmoker.

Basis: Age Nearest Birthday.

Minimum Select Age: 0.

Maximum Select Age: 99.

Minimum Ultimate Age: 25.

Maximum Ultimate Age: 120The package revolves around easy-to-access vectors which are indexed by attained age:

julia> vbt2001.select[35] # vector of rates for issue age 35

0.00036

0.00048

⋮

0.94729

1.0

julia> vbt2001.select[35][35] # issue age 35, attained age 35

0.00036

julia> vbt2001.select[35][50:end] # issue age 35, attained age 50 through end of table

0.00316

0.00345

⋮

0.94729

1.0

julia> vbt2001.ultimate[95] # ultimate vectors only need to be called with the attained age

0.24298Calculate the force of mortality or survival over a range of time:

julia> survival(vbt2001.ultimate,30,40) # the survival between ages 30 and 40

0.9894404665434904

julia> decrement(vbt2001.ultimate,30,40) # the decrement between ages 30 and 40

0.010559533456509618Non-whole periods of time are supported when you specify the assumption (Constant(), Uniform(), or Balducci()) for fractional periods:

julia> survival(vbt2001.ultimate,30,40.5,Uniform()) # the survival between ages 30 and 40.5

0.9887676470262408Parametric Models

Over 20 different models included. Example with the Gompertz model

m = MortalityTables.Gompertz(a=0.01,b=0.2)

m[20] # the mortality rate at age 20

decrement(m,20,25) # the five year cumulative mortality rate

survival(m,20,25) # the five year survival rateActuaryUtilities.jl

A collection of common functions/manipulations used in Actuarial Calculations.

A collection of common functions/manipulations used in Actuarial Calculations.

Quickstart

cfs = [5, 5, 105]

times = [1, 2, 3]

discount_rate = 0.03

present_value(discount_rate, cfs, times) # 105.65

duration(Macaulay(), discount_rate, cfs, times) # 2.86

duration(discount_rate, cfs, times) # 2.78

convexity(discount_rate, cfs, times) # 10.62Features

Financial Maths

duration:- Calculate the

Macaulay,Modified, orDV01durations for a set of cashflows

- Calculate the

convexityfor price sensitivity- Flexible interest rate options via the

FinanceModels.jlpackage. internal_rate_of_returnorirrto calculate the IRR given cashflows (including at timepoints like Excel’sXIRR)breakevento calculate the breakeven time for a set of cashflowsaccum_offsetto calculate accumulations like survivorship from a mortality vector

Key Rate Sensitivities via Automatic Differentiation

Compute exact key rate durations, DV01s, and convexities using ForwardDiff through ZeroRateCurve from FinanceModels.jl — machine-precision sensitivities in a single pass, no bump-and-reprice required.

sensitivities: bundled value, key rate durations, and convexity matrix in a single AD pass- Two-curve decomposition: separate

IR01(risk-free) andCS01(credit spread) sensitivities - Do-block syntax for rate-dependent instruments (callable bonds, floaters)

- Hull-White stochastic model: key rate sensitivities of Monte Carlo expected values

Options Pricing

eurocallandeuroputfor Black-Scholes option prices

Risk Measures

- Calculate risk measures for a given vector of risks:

CTEfor the Conditional Tail Expectation, orVaRfor the percentile/Value at Risk.

Insurance mechanics

duration:- Calculate the duration given an issue date and date (a.k.a. policy duration)

LifeContingencies.jl

Common life contingent calculations with a convenient interface.

Features

- Integration with other JuliaActuary packages such as MortalityTables.jl

- Fast calculations, with some parts utilizing parallel processing power automatically

- Use functions that look more like the math you are used to (e.g.

A,ä) with Unicode support - All of the power, speed, convenience, tooling, and ecosystem of Julia

- Flexible and modular modeling approach

Package Overview

- Leverages MortalityTables.jl for the mortality calculations

- Contains common insurance calculations such as:

Insurance(life,yield): Whole lifeInsurance(life,yield,n): Term life fornyearsä(life,yield):present_valueof life-contingent annuityä(life,yield,n):present_valueof life-contingent annuity due fornyears

- Contains various commutation functions such as

D(x),M(x),C(x), etc. SingleLifeandJointLifecapable- Interest rate mechanics via

FinanceModels.jl - More documentation available by clicking the DOCS badges at the top of this README

Examples

Basic Functions

Calculate various items for a 30-year-old male nonsmoker using 2015 VBT base table and a 5% interest rate

using LifeContingencies

using MortalityTables

using FinanceModels

import LifeContingencies: V, ä # pull the shortform notation into scope

# load mortality rates from MortalityTables.jl

vbt2001 = MortalityTables.table("2001 VBT Residual Standard Select and Ultimate - Male Nonsmoker, ANB")

issue_age = 30

life = SingleLife( # The life underlying the risk

mortality = vbt2001.select[issue_age], # -- Mortality rates

)

yield = FinanceModels.Yield.Constant(0.05)

lc = LifeContingency(life, yield) # LifeContingency joins the risk with interest

ins = Insurance(lc) # Whole Life insurance

ins = Insurance(life, yield) # alternate way to constructWith the above life contingent data, we can calculate vectors of relevant information:

cashflows(ins) # A vector of the unit cashflows

timepoints(ins) # The timepoints associated with the cashflows

survival(ins) # The survival vector

benefit(ins) # The unit benefit vector

probability(ins) # The probability of benefit paymentSome of the above will return lazy results. For example, cashflows(ins) will return a Generator which can be efficiently used in most places you’d use a vector of cashflows (e.g. pv(...) or sum(...)) but has the advantage of being non-allocating (less memory used, faster computations). To get a computed vector instead of the generator, simply call collect(...) on the result: collect(cashflows(ins)).

Or calculate summary scalars:

present_value(ins) # The actuarial present value

premium_net(lc) # Net whole life premium

V(lc,5) # Net premium reserve for whole life insurance at time 5Other types of life contingent benefits:

Insurance(lc,10) # 10 year term insurance

AnnuityImmediate(lc) # Whole life annuity immediate

AnnuityDue(lc) # Whole life annuity due

ä(lc) # Shortform notation

ä(lc, 5) # 5 year annuity due

ä(lc, 5, certain=5,frequency=4) # 5 year annuity due, with 5 year certain payable 4x per year

... # and more!Constructing Lives

SingleLife(vbt2001.select[50]) # no keywords, just a mortality vector

SingleLife(vbt2001.select[50],issue_age = 60) # select at 50, but now 60

SingleLife(vbt2001.select,issue_age = 50) # use issue_age to pick the right select vector

SingleLife(mortality=vbt2001.select,issue_age = 50) # mort can also be a keyword

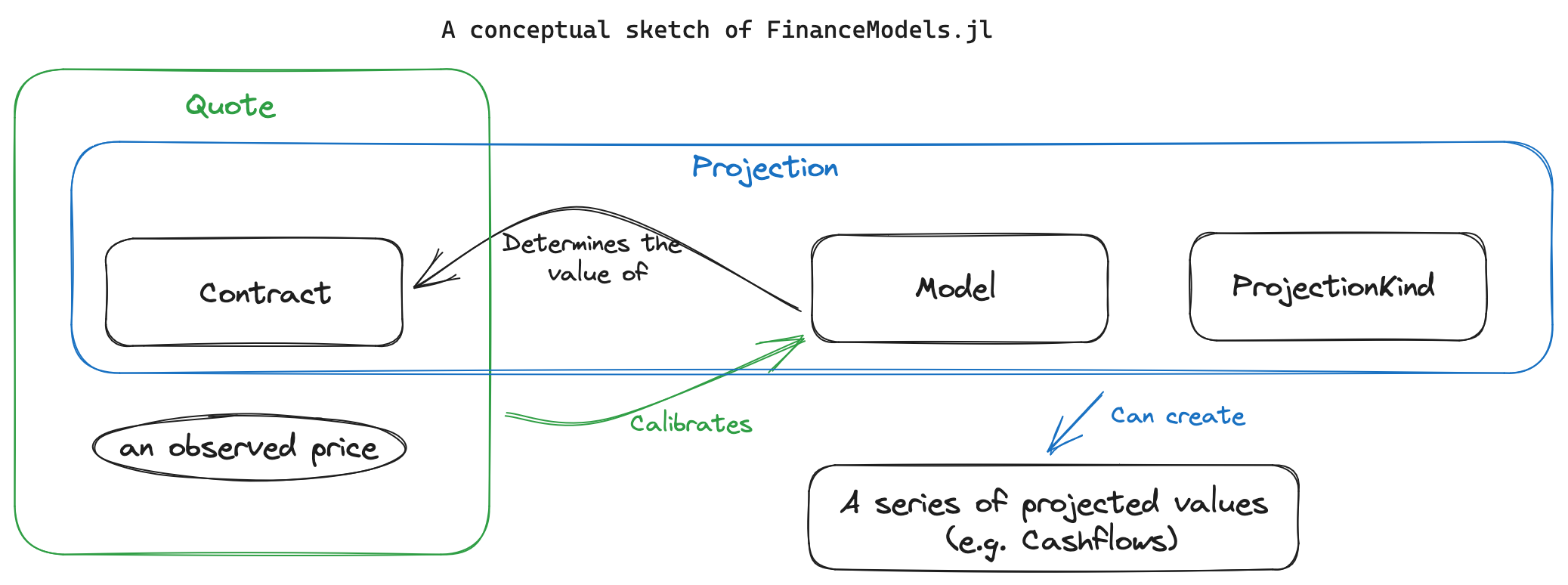

FinanceModels.jl

Flexible and composable yield curves and interest functions.

FinanceModels.jl provides a set of composable contracts, models, and functions that allow for modeling of both simple and complex financial instruments. The resulting models, such as discount rates or term structures, can then be used across the JuliaActuary ecosystem to perform actuarial and financial analysis.

Additionally, the models can be used to project contracts through time: most basically as a series of cashflows but more complex output can be defined for contracts.

QuickStart

using FinanceModels

# a set of market-observed prices we wish to calibrate the model to

# annual effective unless otherwise specified

q_rate = ZCBYield([0.01,0.02,0.03]);

q_spread = ZCBYield([0.01,0.01,0.01]);

# bootstrap a linear spline yield model

model_rate = fit(Spline.Linear(),q_rate,Fit.Bootstrap());

model_spread = fit(Spline.Linear(),q_spread,Fit.Bootstrap());

# the zero rate is the combination of the two underlying rates

zero(model_spread + model_rate,1) # ≈ 0.02

# combining models composes the discount factors multiplicatively

discount(model_spread + model_rate,0,3) ≈ discount(model_spread,0,3) * discount(model_rate,0,3) # true

# compute the present value of a contract (a cashflow of 10 at time 3)

present_value(model_rate,Cashflow(10,3)) # 9.15...Overview of FinanceModels

Often we start with observed or assumed values for existing contracts. We want to then use those assumed values to extend the valuation logic to new contracts. For example, we may have a set of bond yields which we then want to discount a series of insurance obligations.

In the language of FinanceModels, we would have a set of Quotes which are used to fit a Model. That model is then used to discount a new series of cashflows.

That’s just an example, and we can use the various components in different ways depending on the objective of the analysis.

Contracts and Quotes

Contracts are a way to represent financial obligations. These can be valued using a model, projected into a future steam of values, or combined with assumed prices as a Quote.

Included are a number of primitives and convenience methods for contracts:

Existing structs:

CashflowBond.FixedBond.FloatingForward(an obligation with a forward start time)Composite(combine two other contracts, e.g. into a swap)EuroCallCommonEquityOption.Cap,Option.Floor,Option.Swaption(interest rate derivatives)

Commonly, we deal with conventions that imply a contract and an observed price. For example, we may talk about a treasury yield of 0.03. This is a description that implies a Quoteed price for an underling fixed bond. In FinanceModels, we could use CMTYield(rate,tenor) which would create a Quote(price,Bond.Fixed(...)). In this way, we can conveniently create a number of Quotes which can be used to fit models. Such convenience methods include:

ZCBYieldZCBPriceCMTYieldParYieldParSwapYieldForwardYield

FinanceModels offers a way to define new contracts as well.

Cashflows

A Cashflows obligation are themselves a contract, but other contracts can be considered as essentially anything that can be combined with assumptions (a model) to derive a collection of cashflows.

For example, a obligation that pays 1.75 at time 2 could be represented as: Cashflow(1.75,2).

Models

Models are objects that can be fit to observed prices and then subsequently used to make valuations of other cashflows/contracts.

Yield models include:

Yield.Constant- Bootstrapped

Splines Yield.SmithWilsonYield.NelsonSiegelYield.NelsonSiegelSvensson

ZeroRateCurve — Direct Construction

Construct a zero-rate curve directly from rates and tenors without fitting:

- Multiple interpolation options (MonotoneConvex default, Linear, PCHIP, Cubic, Akima)

- ForwardDiff-compatible for AD-based sensitivities (key rate durations, DV01, convexity)

Stochastic Short-Rate Models

ShortRate.Vasicek,ShortRate.CoxIngersollRoss,ShortRate.HullWhitesimulate()for Monte Carlo rate path generationpv_mc()for expected present values under stochastic rates- Closed-form pricing for caps, floors, swaptions (Gaussian models)

Other models include:

BlackScholesMertonderivative valuation

Projections

Most basically, we can project a contract into a series of Cashflows:

julia> b = Bond.Fixed(0.04,Periodic(2),3)

FinanceModels.Bond.Fixed{Periodic, Float64, Int64}(0.04, Periodic(2), 3)

julia> collect(b)

6-element Vector{Cashflow{Float64, Float64}}:

Cashflow{Float64, Float64}(0.02, 0.5)

Cashflow{Float64, Float64}(0.02, 1.0)

Cashflow{Float64, Float64}(0.02, 1.5)

Cashflow{Float64, Float64}(0.02, 2.0)

Cashflow{Float64, Float64}(0.02, 2.5)

Cashflow{Float64, Float64}(1.02, 3.0)However, Projections allow one to combine three elements which can be extended to define any desired output (such as amortization schedules, financial statement projections, or account value rollforwards). The three elements are:

- the underlying contract of interest

- the model which includes assumptions of how the contract will behave

- a

ProjectionKindwhich indicates the kind of output desired (cashflow stream, amortization schedule, etc…)

Fitting Models

Model Method

| |

|------------| |---------------|

fit(Spline.Cubic(), CMTYield.([0.04,0.05,0.055,0.06,0.065],[1,2,3,4,5]), Fit.Bootstrap())

|-------------------------------------------------|

|

Quotes- Model could be

Spline.Linear(),Yield.NelsonSiegelSvensson(),Equity.BlackScholesMerton(...), etc. - Quote could be

CMTYields,ParYields,Option.EuroCall, etc. - Method could be

Fit.Loss(x->x^2),Fit.Loss(x->abs(x)),Fit.Bootstrap(), etc.

This unified way to fit models offers a much simpler way to extend functionality to new models or contract types.

Using Models

After being fit, models can be used to value contracts:

present_value(model,cashflows)Additionally, ActuaryUtilities.jl offers a number of other methods that can be used, such as duration, convexity, price which can be used for analysis with the fitted models.

Rates

Rates are types that wrap scalar values to provide information about how to determine discount and accumulation factors.

There are two Frequency types:

Periodic(m)for rates that compoundmtimes per period (e.g.mtimes per year if working with annual rates).Continuous()for continuously compounding rates.

Examples

Continuous(0.05) # 5% continuously compounded

Periodic(0.05,2) # 5% compounded twice per periodThese are both subtypes of the parent Rate type and are instantiated as:

Rate(0.05,Continuous()) # 5% continuously compounded

Rate(0.05,Periodic(2)) # 5% compounded twice per periodRates can also be constructed by specifying the Frequency and then passing a scalar rate:

Periodic(1)(0.05)

Continuous()(0.05)Conversion

Convert rates between different types with convert. E.g.:

r = Rate(FinanceModels.Periodic(12),0.01) # rate that compounds 12 times per rate period (ie monthly)

convert(FinanceModels.Periodic(1),r) # convert monthly rate to annual effective

convert(FinanceModels.Continuous(),r) # convert monthly rate to continuousArithmetic

Adding, substracting, multiplying, dividing, and comparing rates is supported.

ExperienceAnalysis.jl

Meeting your exposure calculation needs.

Quickstart

df = DataFrame(

policy_id = 1:3,

issue_date = [Date(2020,5,10), Date(2020,4,5), Date(2019, 3, 10)],

end_date = [Date(2022, 6, 10), Date(2022, 8, 10), Date(2022,12,31)],

status = ["claim", "lapse", "inforce"]

)

df.policy_year = exposure.(

ExperienceAnalysis.Anniversary(Year(1)),

df.issue_date,

df.end_date,

df.status .== "claim"; # continued exposure

study_start = Date(2020, 1, 1),

study_end = Date(2022, 12, 31)

)

df = flatten(df, :policy_year)

df.exposure_fraction =

map(e -> yearfrac(e.from, e.to + Day(1), DayCounts.Thirty360()), df.policy_year)

# + Day(1) above because DayCounts has Date(2020, 1, 1) to Date(2021, 1, 1) as an exposure of 1.0

# here we end the interval at Date(2020, 12, 31), so we need to add a day to get the correct exposure fraction.policy_idInt64 |

issue_dateDate |

end_dateDate |

statusString |

policy_year@NamedTuple{from::Date, to::Date, policy\_timestep::Int64} |

exposure_fractionFloat64 |

|---|---|---|---|---|---|

| 1 | 2020-05-10 | 2022-06-10 | claim | (from = Date(“2020-05-10”), to = Date(“2021-05-09”), policy_timestep = 1) | 1.0 |

| 1 | 2020-05-10 | 2022-06-10 | claim | (from = Date(“2021-05-10”), to = Date(“2022-05-09”), policy_timestep = 2) | 1.0 |

| 1 | 2020-05-10 | 2022-06-10 | claim | (from = Date(“2022-05-10”), to = Date(“2023-05-09”), policy_timestep = 3) | 1.0 |

| 2 | 2020-04-05 | 2022-08-10 | lapse | (from = Date(“2020-04-05”), to = Date(“2021-04-04”), policy_timestep = 1) | 1.0 |

| 2 | 2020-04-05 | 2022-08-10 | lapse | (from = Date(“2021-04-05”), to = Date(“2022-04-04”), policy_timestep = 2) | 1.0 |

| 2 | 2020-04-05 | 2022-08-10 | lapse | (from = Date(“2022-04-05”), to = Date(“2022-08-10”), policy_timestep = 3) | 0.35 |

| 3 | 2019-03-10 | 2022-12-31 | inforce | (from = Date(“2020-01-01”), to = Date(“2020-03-09”), policy_timestep = 1) | 0.191667 |

| 3 | 2019-03-10 | 2022-12-31 | inforce | (from = Date(“2020-03-10”), to = Date(“2021-03-09”), policy_timestep = 2) | 1.0 |

| 3 | 2019-03-10 | 2022-12-31 | inforce | (from = Date(“2021-03-10”), to = Date(“2022-03-09”), policy_timestep = 3) | 1.0 |

| 3 | 2019-03-10 | 2022-12-31 | inforce | (from = Date(“2022-03-10”), to = Date(“2022-12-31”), policy_timestep = 4) | 0.808333 |

Available Exposure Basis

ExperienceAnalysis.Anniversary(period)will give exposures periods based on the first dateExperienceAnalysis.Calendar(period)will follow calendar periods (e.g. month or year)ExperienceAnalysis.AnniversaryCalendar(period,period)will split into the smaller of the calendar or policy period.

Where period is a Period Type from the Dates standard library.

Calculate exposures with exposure(basis, from, to, continued_exposure; study_start, study_end).

continued_exposureindicates whether the exposure should be extended through the full exposure period rather than terminate at thetodate.

EconomicScenarioGenerators.jl

Easy-to-use scenario generation that’s FinanceModels.jl compatible.

Models

Interest Rate Models

VasicekCoxIngersollRossHullWhite

EquityModels

BlackScholesMerton

Interest Rate Model Examples

Vasicek

m = Vasicek(0.136,0.0168,0.0119,Continuous(0.01)) # a, b, σ, initial Rate

s = ScenarioGenerator(

1, # timestep

30, # projection horizon

m, # model

)This can be iterated over, or you can collect all of the rates like:

rates = collect(s)or

for r in s

# do something with r

endAnd the package integrates with FinanceModels.jl:

YieldCurve(s)

will produce a yield curve object:

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀Yield Curve (FinanceModels.Yield.Spline)⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

┌────────────────────────────────────────────────────────────┐

0.03 │⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠤⠤⠔⠒⠉⠉⠒⠒⠒⠒⠒⠤⣄⣀│ Zero rates

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠤⠒⠒⠉⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠔⠊⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠔⠋⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢀⣀⣀⠀⠀⣀⡤⠖⠊⠉⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠤⠖⠋⠁⠀⠀⠉⠉⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⠔⠋⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

Continuous │⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⡤⠒⠓⠦⠤⠖⠉⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⢰⠋⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⣀⠖⠢⡀⡰⠃⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠉⠉⠁⠀⠀⠉⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

0 │⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

└────────────────────────────────────────────────────────────┘

⠀0⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀time⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀30⠀